QLCredit represents a shift in how people access money, manage financial risk, and build credit in a world increasingly shaped by algorithms and mobile platforms. Instead of relying solely on traditional banks, paperwork, and long waiting periods, users are turning to digital credit services that promise speed, accessibility, and insight into personal financial behavior.

At its core, QLCredit is positioned as a digital lending and credit-management platform. It offers fast approvals, direct disbursement of funds, and built-in tools that allow users to monitor credit health and financial behavior. For people who have limited credit history, irregular income, or have been excluded from traditional banking, platforms like QLCredit provide a new entry point into formal financial systems.

This transformation reflects broader changes in the global economy. Work is becoming more flexible, income is more fragmented, and traditional financial institutions are often poorly suited to evaluate modern financial lives. By using data-driven assessments rather than rigid scoring systems, QLCredit attempts to capture a more complete picture of how people earn, spend, and repay.

However, this new model also carries risks. Faster access to money can mean faster accumulation of debt. Algorithmic decisions can introduce bias or opacity. And the emotional ease of tapping a screen to borrow money can distance users from the long-term consequences of repayment. Understanding QLCredit therefore requires looking not only at how it works, but what it reveals about how finance itself is changing.

Body

Digital lending platforms emerged from the convergence of mobile technology, big data, and shifting consumer expectations. People now expect financial services to be as fast and intuitive as messaging apps or online shopping. QLCredit reflects this expectation by offering streamlined onboarding, automated assessment, and near-instant loan decisions.

Instead of focusing only on traditional credit scores, QLCredit evaluates patterns of income, spending, repayment behavior, and other financial signals. This allows the system to extend credit to individuals who might not meet conventional criteria but who demonstrate financial responsibility through other indicators.

This approach broadens access to credit while also redefining how financial trust is established. Trust is no longer built through long relationships with a single institution but through continuous streams of data that reflect behavior in real time. This redefinition has profound implications for privacy, autonomy, and fairness.

Traditional banks are structured around stability, regulation, and risk minimization. Digital platforms are structured around speed, flexibility, and user experience. QLCredit occupies a middle ground where financial authority shifts from institutions to systems and interfaces. The platform becomes not just a lender but a mediator between individuals and financial systems.

Table

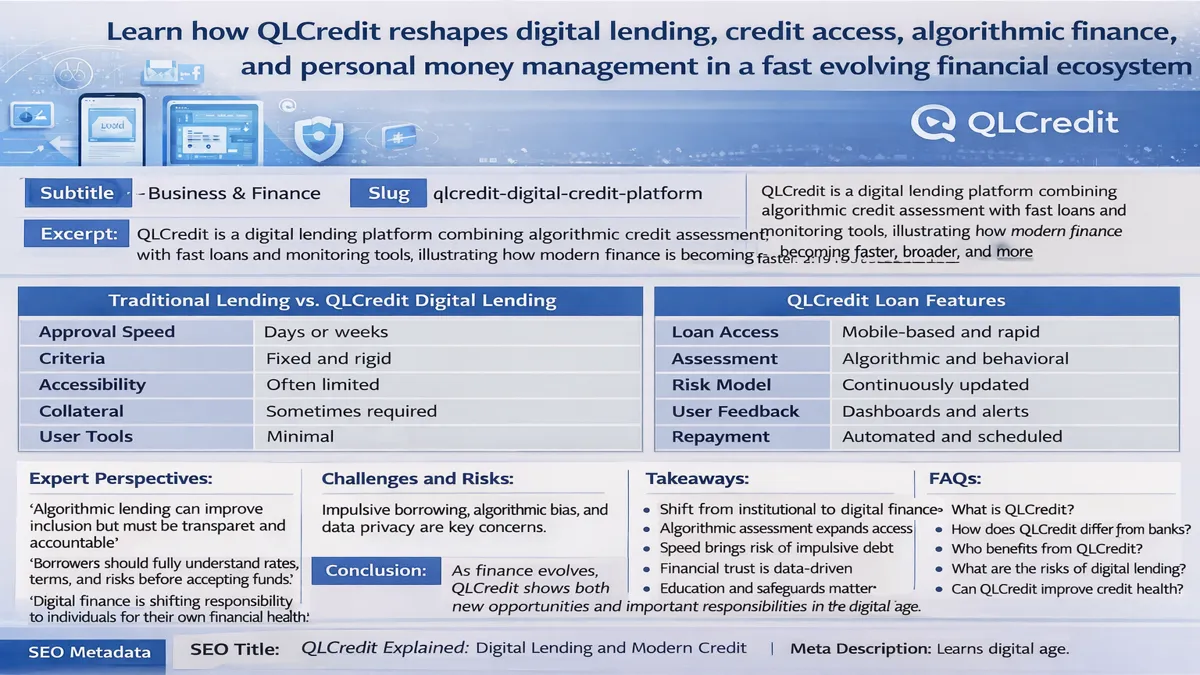

Feature | Traditional Lending | QLCredit Digital Lending

Approval Speed | Days or weeks | Minutes or hours

Criteria | Fixed and rigid | Data-driven and adaptive

Accessibility | Often limited | Broad and low-barrier

Collateral | Sometimes required | Rarely required

User Tools | Minimal | Real-time monitoring

Table

Aspect | Description

Loan Access | Mobile-based and rapid

Assessment | Algorithmic and behavioral

Risk Model | Continuously updated

User Feedback | Dashboards and alerts

Repayment | Automated and scheduled

Expert Perspectives

Financial researchers note that algorithmic lending can improve inclusion but must be transparent and accountable. When people do not understand how decisions are made, trust can erode and errors become harder to challenge.

Consumer advocates emphasize that speed should never replace clarity. Borrowers must fully understand interest rates, repayment schedules, and consequences before accepting funds.

Technology analysts argue that platforms like QLCredit represent a broader cultural shift toward self-managed finance, where individuals take on more responsibility for monitoring, planning, and understanding their financial lives.

Challenges and Risks

The convenience of digital credit can encourage impulsive borrowing. Without the friction of paperwork or human interaction, users may take loans without fully considering long-term impacts.

There is also the risk of algorithmic bias, where certain populations are unintentionally disadvantaged by data patterns that reflect historical inequality.

Finally, data privacy remains a central concern. As financial behavior becomes data, it becomes valuable, tradable, and vulnerable. Protecting that data is as important as protecting money itself.

Takeaways

- QLCredit reflects the shift from institutional to digital finance

- Algorithmic assessment expands access but raises transparency concerns

- Speed improves convenience but increases risk of impulsive debt

- Financial trust is increasingly built through data rather than relationships

- Digital lending reshapes how individuals interact with money

- Education and safeguards are essential for responsible use

Conclusion

QLCredit is not just a financial product. It is a signal of how money, trust, and technology are becoming intertwined. It shows how access to credit is expanding beyond traditional boundaries while simultaneously introducing new risks and responsibilities.

As financial systems become more automated, individuals gain more control but also bear more burden. They must understand not only how to use financial tools but how those tools shape behavior, opportunity, and vulnerability.

The future of finance will not be defined solely by banks or platforms, but by how societies choose to balance innovation with protection, speed with understanding, and access with responsibility. QLCredit offers a glimpse into that future — one that is faster, broader, and more complex than anything before it.

FAQs

What is QLCredit

QLCredit is a digital lending and credit-monitoring platform that uses data to assess financial behavior and provide fast access to loans.

How does QLCredit differ from banks

It uses algorithmic assessment, mobile interfaces, and rapid approvals instead of branch-based, manual processes.

Who can benefit from QLCredit

People with limited credit history, freelancers, and those underserved by traditional banks may benefit most.

What are the risks of digital lending

Impulsive borrowing, unclear terms, data privacy issues, and algorithmic bias are key risks.

Can QLCredit improve credit health

Responsible use and repayment can support better financial behavior, but misuse can worsen debt.